|

Considering that the worth of the home is an essential aspect in understanding the threat of the loan, figuring out the value is a key consider home mortgage financing. The value might be identified Find more info in various ways, however the most typical are: Real or transaction worth: this is generally taken to be the purchase cost of the residential or commercial property. Appraised or surveyed worth: in a lot of jurisdictions, some kind of appraisal of the worth by a certified professional is common. what lenders give mortgages after bankruptcy. There is frequently a requirement for the loan provider to obtain a main appraisal. Approximated worth: lenders or other parties might use their own internal price quotes, especially in jurisdictions where no official appraisal procedure exists, however likewise in some other circumstances. Common denominators consist of payment to earnings (home loan payments as a percentage of gross or net earnings); debt to earnings (all debt payments, including home mortgage payments, as a percentage of income); and numerous net worth procedures. In lots of countries, credit report are utilized in lieu of or to supplement these procedures. the specifics will vary from place to area. Income tax incentives typically can be used in forms of tax refunds or tax reduction plans. how to get a timeshare The first suggests that income tax paid by private taxpayers will be refunded to the degree of interest on home loan taken to get house. Some lenders might likewise need a possible debtor have several months of "reserve possessions" offered. In other words, the borrower may be needed to show the availability of enough assets to pay for the real estate expenses (including home loan, taxes, and so on) for a period of time in the occasion of the job loss or other loss of income. Lots of nations have a concept of basic or adhering home mortgages that specify a viewed appropriate level of risk, which may be official or informal, and might be strengthened by laws, federal government intervention, or market practice. For example, a standard mortgage might be considered to be one without any more than 7080% LTV and no more than one-third of gross earnings going to mortgage debt. An Unbiased View of Blank Have Criminal Content When Hacking Regarding Mortgages

In the United States, a conforming mortgage is one which meets the established rules and treatments of the two significant government-sponsored entities in the real estate finance market (including some legal requirements). In contrast, lending institutions who choose to make nonconforming loans are exercising a greater risk tolerance and do so understanding that they deal with more difficulty in reselling the loan. Regulated loan providers (such as banks) might undergo limitations or higher-risk weightings for non-standard home mortgages. For example, banks and home mortgage brokerages in Canada deal with restrictions on providing more than 80% of the residential or commercial property value; beyond this level, home mortgage insurance coverage is normally needed. In some countries with currencies that tend to diminish, foreign currency home loans are common, enabling loan providers to provide in a steady foreign currency, whilst the debtor handles the currency risk that the currency will diminish and they will therefore need to transform greater quantities of the domestic currency to pay back the loan. Total Payment = Loan Principal + Costs (Taxes & charges) + Total interests. Repaired Interest Rates & Loan Term In addition to the 2 basic ways of setting the cost of a mortgage (repaired at a set rates of interest for the term, or variable relative to market rates of interest), there are variations in how that expense is paid, and how the loan itself is paid back. There are likewise different mortgage payment structures to fit different kinds of customer. The most typical method to pay back a secured home loan is to make regular payments towards the principal and interest over a set term. [] This is typically referred to as (self) in the U.S (how did clinton allow blacks to get mortgages easier). and as a in the UK. Certain information may specify to different places: interest might be computed on the basis of a 360-day year, for instance; interest may be intensified daily, yearly, or semi-annually; prepayment penalties may apply; and other elements. There might be legal limitations on particular matters, and consumer defense laws may define or prohibit certain practices. In the UK and U.S., 25 to thirty years is the typical optimum term (although much shorter periods, such as 15-year home loan, prevail). Mortgage payments, which are usually made regular monthly, include a payment of the principal and an interest element. The amount approaching the principal in each payment differs throughout the regard to the home loan. The Facts About Reddit How Long Do Most Mortgages Go For Uncovered

Towards the end of the home mortgage, payments are mostly for principal. In this way, the payment amount determined at outset is computed to make sure the loan is repaid at a defined date in the future. This offers debtors assurance that by preserving payment the loan will be cleared at a defined date if the interest rate does not alter. Similarly, a mortgage can be ended prior to its scheduled end by paying some or all of the rest prematurely, called curtailment. An amortization schedule is normally exercised taking the principal left at the end of each month, multiplying by the monthly rate and after that subtracting the regular monthly payment (when did subprime mortgages start in 2005). This is normally generated by an amortization calculator utilizing the following formula: A = P r (1 + r) n (1 + r) n 1 \ displaystyle A =P \ cdot \ frac r( 1+ r) n (1+ r) n -1 where: A \ displaystyle is the routine amortization payment P \ displaystyle P is the principal quantity borrowed r \ displaystyle r is the rate of interest expressed as a fraction; for a monthly payment, take the (Annual Rate)/ 12 n \ displaystyle n is the variety of payments; for monthly payments over 30 years, http://alexisnfpl042.cavandoragh.org/the-smart-trick-of-how-a-simple-loan-works-for-mortgages-that-nobody-is-talking-about 12 months x 30 years = 360 payments. This type of home loan is typical in the UK, especially when connected with a regular investment plan. With this plan regular contributions are made to a different financial investment plan designed to build up a lump sum to repay the home mortgage at maturity. This type of plan is called an investment-backed mortgage or is frequently related to the type of plan utilized: endowment mortgage if an endowment policy is used, similarly a personal equity strategy (PEP) mortgage, Individual Cost Savings Account (ISA) home mortgage or pension mortgage. Investment-backed mortgages are seen as greater danger as they depend on the financial investment making adequate go back to clear the debt. Until recently [] it was not unusual for interest only home mortgages to be arranged without a repayment lorry, with the debtor betting that the home market will rise sufficiently for the loan to be repaid by trading down at retirement (or when rent on the property and inflation integrate to go beyond the rate of interest) []. The problem for lots of people has actually been the reality that no repayment vehicle had actually been carried out, or the vehicle itself (e. g. endowment/ISA policy) carried out inadequately and therefore insufficient funds were offered to pay back balance at the end of the term. Moving on, the FSA under the Mortgage Market Review (MMR) have stated there must be rigorous criteria on the repayment automobile being utilized.

0 Comments

The home mortgage is between the lending institution and the property owner. In order to own the home, the debtor agrees to a regular monthly payment over the payment period agreed upon. As soon as the property owner pays the home mortgage in full the lending institution will approve deed or ownership. Your regular monthly mortgage payment includes a portion of your loan principal, interest, residential or commercial property taxes and insurance coverage. The majority of home loan loans last in between 10, 15 or 30 years and are either fixed-rate or adjustable-rate. If you choose a fixed-rate home loan, your rate of interest will remain the exact same throughout your loan. But if your home loan is adjustable, your home mortgage's interest rate will depend on the marketplace each year, suggesting that your month-to-month payment might vary. If a house owner does not make payments on their home loan, they could deal with late charges or other credit penalties. The mortgage also gives the lending institution the right to acquire and sell the property to another person, and the property owner can face other charges from the lending institution. All in all, home loans are an excellent, inexpensive alternative for acquiring a house without the concern of paying in full upfront. Indicators on Why Do Mortgage Companies Sell Mortgages To Other Banks You Need To Know

Refinancing can be a clever option for house owners aiming to decrease their existing interest rate or regular monthly payments. It is important for homeowners to understand the details of their primary mortgage in addition to the re-finance terms, plus any associated expenses or fees, to ensure the decision makes monetary sense. In basic, homebuyers with great credit report of 740 or greater can expect lower interest rates and more choices, including jumbo loans. Your rate will also be determined based upon the loan-to-value ratio, which thinks about the percentage of the house's value that you're paying through the loan. A loan-to-value ratio greater than 80% could be thought about risky for lenders and result in greater interest rates for the home buyer. Nevertheless, remember that these interest rates are a typical based on users with high credit history. Presently, an excellent rates of interest will be about 3% to 3. 5%, though these rates are historically low. The Federal Reserve affects mortgage rates by raising and lowering the federal funds rate. What Are The Lowest Interest Rates For Mortgages Fundamentals Explained

As you buy a lending institution, your real estate representative may have a few favored choices, however it all comes down to what works best for you. The Federal Trade Commission (FTC) recommends getting quotes from different loan providers and calling several times to get the finest rates. Be sure to ask about the interest rate (APR) and interest rates. Some common costs might include hilton head timeshare appraisal and processing costs. Be sure to inquire about any costs that are unknown and if they can be worked https://www.timesharestopper.com/blog/why-are-timeshares-a-bad-idea/ out. For the very best rates, you should attempt to get preapproved by several loan providers before making a decision. Buying a home is a huge step and your mortgage lender plays a crucial function while doing so. Most importantly, check out any documents and the great print so there aren't any unpredicted fees or expectations. The Consumer Financial Defense Bureau has a loan quote explainer to help you double-check all the information agreed upon in between you and your loan provider. When requesting a home mortgage, the kind of loan will generally figure out the length of time you'll have your home loan. The Basic Principles Of Who Has The Best Interest Rates On Mortgages

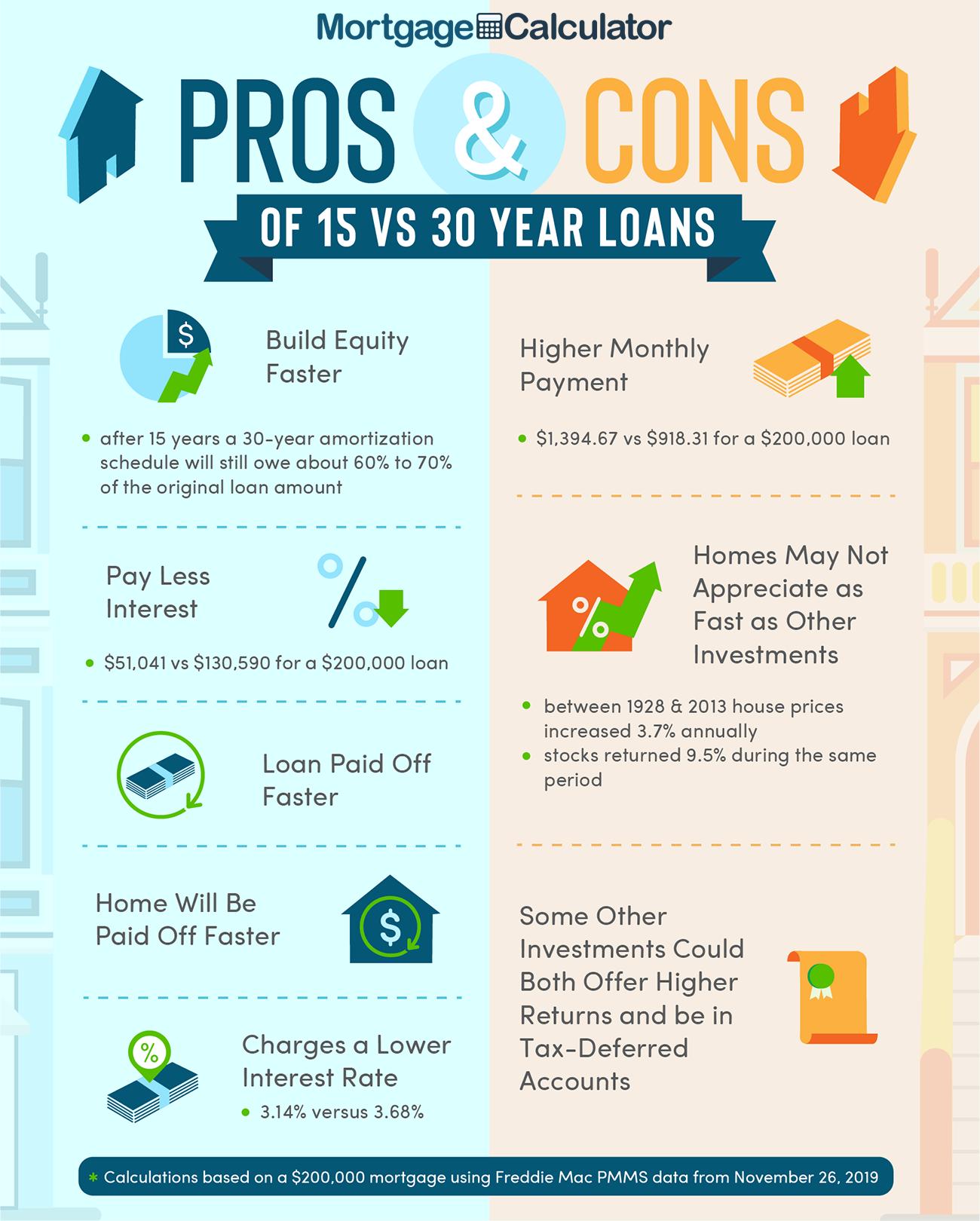

With a much shorter term, you'll pay a higher monthly rate, though your overall interest will be lower than a 30-year loan. If you have a high month-to-month earnings along with long-term stability for the foreseeable future, a 15-year loan would make good sense to conserve cash in the long-term. Nevertheless, a 30-year term would be much better for somebody who needs to make lower regular monthly payments. By excellent general rule, you should only be spending 25% to 30% of your regular monthly earnings on housing monthly. The Federal Real Estate Administration and Fannie Mae set loan limits for traditional loans. By law, all mortgage loans have a maximum limit of 115% of median home costs. Presently, the loan limit for a single system within the United States is $510,400. Government-insured loans such as FHA have actually similar limitations based on present real estate rates. At the end of 2019, the FHA limit was increased to $331,760 in most parts of the country. VA loan limitations were eliminated in early 2020. There's a huge distinction between the yearly portion rate (APR) and the rate of interest. The What Are Today's Interest Rates On Mortgages Diaries

Here's the big distinction your APR is a breakdown of whatever you're paying during the home purchasing procedure, consisting of the interest rate and any additional costs. APRs might also consist of closing costs and other lending institution costs. APRs are normally higher than rate of interest since it's a breakdown of all charges you'll be paying, while the rates of interest is entirely the general expense of the loan you'll pay. It's the total quantity you're spending for obtaining the cash. On the other hand, the rate of interest is the rate, without charges, that you're being charged for the loan. The rates of interest is based upon elements consisting of the loan amount you concur to pay and your credit history. Interest rates can likewise differ depending on the kind of loan you select and your state, in addition to some other factors. What may not be readily apparent, though, is how changes in your rate can make a major impact. Let's have a look at what would take place if a 30-year fixed-rate home loan of $350,000 went up by just 0. 1%. Utilizing a mortgage rate calculator, you can see your monthly home loan payment would increase from $1,773 to $1,794 if your rate increased from 4. Things about What Are The Current Interest Rates For Mortgages

6%. That doesn't seem so bad, right?However, take a look at the overall interest you'll accrue and pay during the life of the 30-year home mortgage. That tiny 0. 1% boost in your rate is the distinction between $288,422 in interest payments and $295,929. And if your fixed-rate home loan was an ARM rather, that gap might be substantially higher tens of thousands higher.

Citizens BankOnline tools6203. 5% 13TD BankGovernment loans7003% 19Bank of AmericaDiscounts for existing customers6203% 5% * 50Quicken LoansFlexible terms5803. 5% 50New American FundingNo minimum payment6200% 48J. G. WentworthLow-income options5803% 45USAA MortgageCustomer service6200% 50SunTrust MortgageDiverse loan types6203% 50ChaseOnline home loan tracking6203% 40 The Coronavirus pandemic has triggered significant decreases to home mortgage rates as need plummeted. With Americans sequestered in their houses, the marketplace has stalled without any new properties, no brand-new sales, and no brand-new buyers. Joblessness stays at an all-time high, however renewed commerce should produce brand-new buyers and continue to increase demand. As the weeks continue to pass, professionals forecast the market will slowly begin to rebound, and we will see mortgage rates rise in reaction as the nation continues to recuperate. Unknown Facts About What Will Happen To Mortgages If The Economy Collapses

Tips for Comparing Home Mortgage LendersEven if you elect to get quotes from numerous home loan service providers online, you can likewise check regional home mortgage suppliers. Your local newspaper more than likely provides quotes for a few of the most competitive home mortgage lending institutions in your neighborhood. You might find that dealing with a local home mortgage service provider is most practical (what does ltv stand for in mortgages). Points programs can be run by a program operator, or can be part of a vacation club timesharing program. Recently, some exchange business (see Lesson 3 for a conversation of exchange companies) have actually begun developing points programs - what is a timeshare?. An essential worry about points programs is the long-lasting "value" of your points in scheduling lodgings. If you own or are considering buying into a points system, you need to examine the program files carefully to determine what protections you might have versus such losses in exchange power. Points programs and right-to-use resort properties have many typical functions, and the majority of the warns previously described for right-to-use projects likewise apply to points programs.

Through such exchanges, you can obtain timeshare lodgings in preferable trip areas throughout the world. Exchanging also allows you to trip at different times of the year, Discover more even utilizing a fixed week. The simplest exchange technique is to discover a timeshare owner who is interested in exchanging his or her week for your week. Another exchange choice takes place when your timeshare ownership becomes part of an exchange program that includes numerous resorts in various places. In these plans, you can exchange your week for a week at another resort within the group. Numerous timeshare management business that run resorts in different locations provide this kind of exchange service as part of their management services - how to get rid of timeshare legally. The most common exchange approach is through a timeshare exchange business. To do this, you "deposit" your week with the exchange company. As other owners transfer their weeks (and as resorts deposit unsold weeks with the exchange company), the exchange business constructs up an inventory of weeks that are offered for exchanges. The exchange company hence acts as a clearinghouse for individuals making exchanges. Keep in mind that the owner of the week you exchange for will nearly never ever be the individual who receives the week you deposit. The demand for numerous resorts differs seasonally. For example, for people living in the northern hemisphere, beach areas are popular in the summertime, whereas ski resorts are most popular throughout ski seasons. This worth impacts both the price of the system and the quality and kinds of exchanges you can make with the timeshare unit. Resort Condominiums International (RCI) and Interval International (II), the 2 largest exchange business, both divide weeks into three seasons, designated by color. For RCI, the designations are: Red: high demand season White: intermediate need season Blue: low demand season For II, the designations are: Red: high need season Yellow: intermediate need season Green: low demand season The classifications of seasons differ with each resort. Not known Factual Statements About How To Rent A Timeshare Week

You must also understand that even within these seasons, some weeks are in higher need than others. For example, July and August weeks in southern California are usually in greater need than are October weeks, even though all of the weeks are considered high demand weeks. This suggests some red weeks are "redder" than other red weeks. These internal season or date classifications frequently differ from RCI's and II's seasonal classifications for the very same resort. PULL has numerous other posts that offer guidance and details on timesharing. Follow these links to the PULL Suggestions page and the PULL Timeshare Frequently Asked Question page. Timeshare purchases can be divided into purchases of "brand-new" units (purchased from the resort developer) and "resale" systems (purchased from any celebration aside from the developer, such as an owner, a timeshare reselling representative, or a homeowners association). Designers are the entities that produce timeshare projects by developing the resort (or by transforming an existing resort) and selling the systems to buyers. Developers run the range from poorly financed, minimal operations to well-known travel and leisure corporations such as Marriott, Hilton and Disney. Many of the early developers of timeshare jobs were minimal operations, and contributed to the bad picture of timesharing. Sometimes the designer handles both task development and sales. Other times, the designer will schedule a company that specializes in timeshare sales to market and sell the intervals to buyers. To intrigue individuals in participating in a sales discussion, the sales program generally consists of financial rewards to individuals who attend sales discussions. Timeshare sales and marketing costs can easily be 50 percent or more of the designer's list prices. You may be shocked that sales and marketing expenses might be so high, however a good timeshare job can easily support these costs. For instance, think about that a developer can most likely develop and furnish a twobedroom condominium system in most parts of the United States for about $150,000 per unit. If the developer invests half this quantity marketing the units ($250,000 per unit), the building and construction cost and sales and marketing cost together will total $400,000, leaving $100,000 earnings per system. As mentioned formerly, a resale happens when a non-developer owner of a timeshare week offers that week to another party. Some resorts have on-site resale agents who accept listings from owners who want to offer their timeshare units. There are a variety of reasons that individuals offer timeshares they own, consisting of deaths, divorces, monetary emergency situations, changes in individual trip habits, and, sadly, people learning that timesharing does not work for their way of life. What Happens If You Stop Paying Maintenance Fees On A Timeshare Can Be Fun For Everyone

As was suggested in the above discussion of developer sales, Helpful hints 50 percent or more of a designer's prices represents the cost of the designer's sales and marketing program. A personal individual can't do the same things a developer does to stimulate demand for their week. Usually all a private individual can do is try to let possible purchasers understand that they have a week they would like to offer, and see what price the marketplace will bear. As a rough guide, resale costs more closely reflect the cost of the unit absent the sales and marketing program, or approximately 50 percent of the new prices. Resale prices for a couple of timeshare systems have actually held above this level; these are typically high quality resorts in places with high need and limited supply. Conversely, some timeshare systems are basically worthless. Because there is no main clearinghouse for resale rates, you often can not approximate a resale cost based on past sales. Doing not have historic sales data, you should simply recognize that the worth of a resale unit is whatever price a purchaser and a seller settle on. Although list prices info for deeded residential or commercial properties will typically be gathered by a regional company as part of the deed recording process, unless you live near the deed recording office you will not easily have the ability to evaluate these records - how to cancel a timeshare contract. TUG likewise has a historical sales database, consisting of data offered by TUG members, that may be useful. Underneath the surface, however, there are Browse around this site a lot of moving parts. Even little options in how you prepare for homeownership, or what kind of home mortgage you get, can have big repercussions http://jasperfbos283.xtgem.com/not%20known%20details%20about%20how%20many%20mortgages%20can%20you%20have%20at%20one%20time for your savings account. It's all about dealing with a loan provider you feel comfy with and you trust to understand your scenario, says Kevin Parker, vice president of field home mortgage at Navy Federal Cooperative Credit Union. In just the previous few months, the method you go about purchasing a home has changed, as the industry has adjusted to a significantly remote process. In the middle of a pandemic and economic downturn, it's even more essential to understand what you'll need for a smooth home loan process.Get Your Financial resources in OrderGet Preapproved for a Home mortgagePurchase the Right Home Mortgage and LenderNavigate the Underwriting and Closing ProcessPurchasing a house, particularly if it's your first time, can be a complex and demanding procedure. Dealing with an experienced genuine estate agent and lender or home loan broker can assist you navigate the process. Preparing your financial resources is increasingly essential provided how wary lenders have ended up being. Sean Moss, the director of operations for Down Payment Resource, an aggregator of homebuyer help programs, advises you start the process by talking with a loan officer. You must concentrate on 2 things: Structure your credit and conserving your money. Having more cash on hand and a stronger credit rating will assist you have the ability to manage a broader variety of homes, making the time it requires to shore up both well worth it. Your approval odds and mortgage alternatives will be much better the higher your credit rating. The 5-Minute Rule for What Is The Interest Rate On Mortgages Today

The lower your credit report, the higher your home mortgage interest rate (and hence funding costs). how do down payments work on mortgages. So strengthening your credit by paying your bills on time and settling financial obligation can make a home loan more budget friendly. Two of the finest things you can do to get the very best home loan rates: putting in the time to develop your credit history and saving for a deposit of at least 20%. You'll need a huge chunk of money to pay upfront closing expenses and a deposit. Closing costs consist of all costs associated with processing the home loan and average 3% -6% of the purchase price. A healthy down payment will be 20% of the home's worth, though it is possible to purchase a house with a smaller sized deposit, specifically for particular types of loans. But do not let that number hinder you from making own a home a reality. There are ways to bring it down. There are regional and regional programs that use closing cost and deposit assistance for qualified buyers, generally newbie homeowners or purchasers with low-to-moderate income. This assistance typically is in the kind of a grant, low or no-interest loan, or a forgivable loan. This helps the customer keep cash in cost savings so they're better prepared for emergency situations and the extra costs of homeownership. Getting preapproved for a home loan provides you an excellent concept of how much you can obtain and reveals sellers you are a qualified purchaser. To get a preapproval, a lender will inspect your credit Have a peek here history and proof of your earnings, possessions, and work. How Which Of The Following Statements Is Not True About Mortgages can Save You Time, Stress, and Money.

A lot of preapproval letters are legitimate for 60-90 days, and when it comes time to get a home mortgage all of your information will require to be reverified. Also, don't confuse preapproval with prequalification. A prequalification is a fast price quote of what you can borrow based on the numbers you share and does not require any documents. When searching for a home mortgage it's an excellent idea to look around to compare rates and costs for 2-3 lending institutions. When you send a home mortgage application, the lending institution is required to provide you what is understood as a loan quote within three organization days. Every loan estimate contains the very same details, so it's easy to compare not only rate of interest, however also the in advance costs you'll need to pay. It's also essential to understand the different mortgage terms. The term is the amount of time the loan is paid back over typical home loan terms are 10, 15, and 30 years. This has a big influence on your month-to-month payment and how much interest you pay over the life of the loan. A shorter-term loan will conserve you cash on interest. This is since shorter loans normally have lower rate of interest, and you're paying the loan off in a much shorter amount of time. To comprehend how various terms impact your bottom line, utilize our home loan calculator to see how the regular monthly payment and the total interest you'll pay modifications.

A Biased View of When Did 30 Year Mortgages Start

There are fixed-rate loans, which have the exact same interest throughout of the mortgage, and adjustable rate home mortgages, which have an interest rate that alters with market conditions after a set number of years. There are also what are known as government-backed loans and conventional loans. A government-insured mortgage is less dangerous for the lending institution, so it might be much easier to get approved for, but comes with extra limitations. Department of Agriculture (USDA) are only released for properties located in a certifying rural area. Likewise, the personal home mortgage insurance coverage requirement is generally dropped from traditional loans when the loan-to-value ratio (LTV) is up to 80%. But for USDA and Federal Real Estate Administration (FHA) loans, you'll pay a variation of home loan insurance coverage for the life of the loan. Your monetary health will be carefully inspected throughout the underwriting process and before the mortgage is provided or your application is turned down. You'll require to provide recent documentation to confirm your work, earnings, assets, and debts. You may likewise be required to submit letters to discuss things like employment spaces or to record gifts you receive to aid with the down payment or closing expenses. Prevent any huge purchases, closing or opening brand-new accounts, and making abnormally large withdrawals or deposits. As part of closing, the lending institution will need an appraisal to be completed on the home to validate its value. You'll also require to have a title search done on the residential or commercial property and safe and secure lender's title insurance coverage and homeowner's insurance coverage. Fascination About Who Does Usaa Sell Their Mortgages To

Lenders have ended up being more rigorous with whom they want to loan cash in reaction to the pandemic and occurring financial recession. Minimum credit report requirements have increased, and loan providers are holding borrowers to higher requirements. For example, loan providers are now verifying employment prior to the loan is completed, Parker states. Lots of states have fasted lane approval for making use of digital or mobile notaries, and virtual house trips, " drive-by" appraisals, and remote closings are becoming more typical - which credit report is used for mortgages. While numerous lending institutions have fine-tuned the logistics of authorizing mortgage remotely, you may still experience delays at the same time. All-time low home loan rates have caused a boom in refinancing as existing homeowners seek to save. Spring is typically a hectic time for the property market, however with the shutdown, numerous buyers had to put their house hunting on time out. As these purchasers go back to the marketplace, loan pioneers are becoming even busier. After the reverse home mortgage earnings settle the existing home mortgage, the foreclosure stops and you won't have to make anymore month-to-month payments. Sounds pretty excellent, best? However there are downsides to utilizing a reverse home loan in this method. One disadvantage is that the borrower loses some or the majority of the equity that's developed up for many years. Likewise, the reverse home mortgage loan provider can call the loan due if and when one of the following events takes place: The customer permanently vacates the house. The debtor moves out of the house short-term due to a physical or psychological illness, and is chosen over a year. The borrower sells the house or deeds the home to a new owner. (If a certified non-borrowing partner still resides in the home, the lending institution can't call the loan due under particular scenarios). The customer doesn't satisfy the home mortgage requirements, like paying real estate tax, having house owners' insurance on the home, and keeping the home in great condition. what metal is used to pay off mortgages during a reset. As soon as the lending institution calls the loan due, the loan needs to be paid back or the lending institution will foreclose. A reverse home loan is just one way to avoid a foreclosure. A few other choices to think about are: refinancing the existing mortgage getting a home mortgage modification, or selling the house rci timeshare review and transferring to more economical lodgings. The Consumer Financial Security Bureau offers a helpful reverse home mortgage conversation guide and advises customers who are considering securing a reverse mortgage to consider all other alternatives - mortgages what will that house cost. About How Do Reverse Mortgages Get Foreclosed Homes

Although you'll need to complete a counseling session with a HUD-approved counselor if you wish to get a HECM, it's also extremely recommended that you consider speaking with a financial coordinator, an estate planning attorney, or a customer defense legal representative prior to getting this type of loan - who has the lowest apr for mortgages. A new thorough investigation on foreclosure actions connected to reverse home loans published late Tuesday by USA Today paints a bleak image surrounding the activities and practices of the reverse mortgage market, but also relates some doubtful and obsolete details in essential locations highlighted by the investigation, according to industry participants who consulted with RMD.

Referring to a wave of reverse mortgage foreclosures that mainly affected metropolitan African-American neighborhoods as a "stealth aftershock of the Great Economic crisis," the investigative short article concentrates on nearly 100,000 foreclosed reverse mortgages as having "stopped working," and impacting the virginia beach timeshare cancellation financial futures of the debtors, adversely affecting the home values in the communities that surround the foreclosed properties. |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

March 2022

Categories |

RSS Feed

RSS Feed